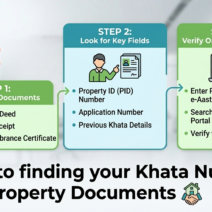

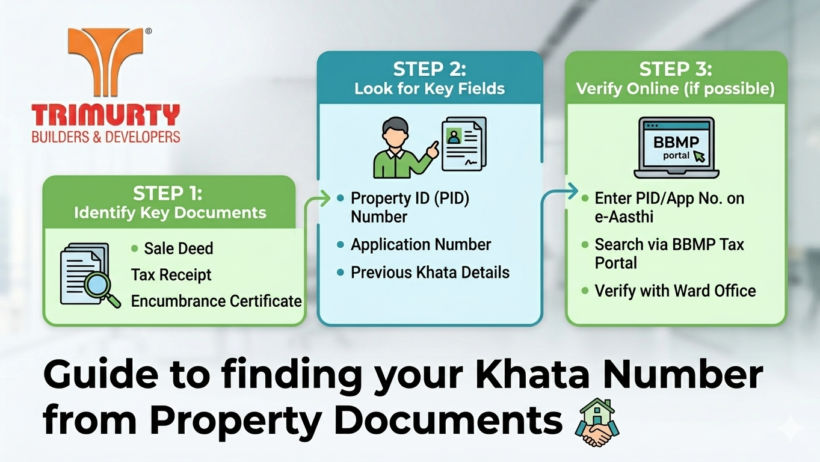

Property Investment How to find Khata Number using Property Documents 0Marketing TrimurtyMarch 27, 202610 min read

Property Investment Buy a Vastu-Compliant Home This Festive Season – Trimurty’s Expert Guide 0October 3, 20172 min read

Property Investment Trimurty’s Arabella – Jaipur’s Premier Green Luxury Residences 0September 27, 20172 min read

Property Investment RERA: A Blessing for Buyers & a Ban for Unscrupulous Developers 0September 20, 20172 min read

Property Investment Why Trimurty Ariana is the Best Residential Choice in Jaipur 0September 15, 20172 min read