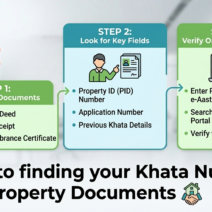

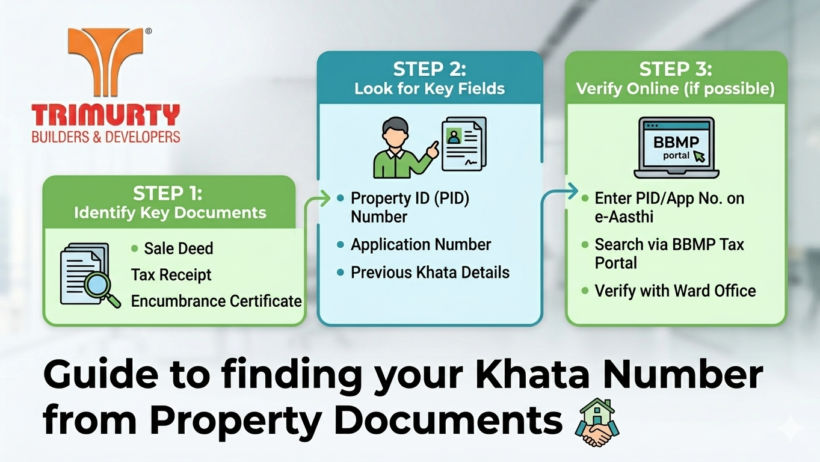

Property Investment How to find Khata Number using Property Documents 0Marketing TrimurtyMarch 27, 202610 min read

Property InvestmentReal EstateTrimurty Jaipur the Hot Market for Real Estate Investment 0March 2, 20172 min read

Apartment LivingNews & EventsProperty InvestmentReal EstateTips and TricksTrimurty How to Make your Guest Room More Comfortable in 5 Simple Ways 0February 25, 20172 min read

Apartment LivingNews & EventsProperty InvestmentReal EstateTrimurty Trimurty’s Ariana @ Jagatpura, Jaipur’s New Property Hub 0February 13, 20172 min read

Apartment LivingProperty InvestmentReal EstateTrimurty Why investing in Green Home is Profitable? 0January 30, 20172 min read